Pathways to structural transformation of the Ghanaian economy—and some roadblocks

Feature Article

Ghanaian economy

Ghanaian economy

While Ghana’s economic growth over the last decade has been comparatively strong—annual economic growth averaged approximately 6.8 per cent for the period 2010-2019—this growth has largely been driven by minerals and crude oil production rather than by the manufacturing sector, which has a higher propensity to create more jobs. Indeed, Ghana’s efforts to encourage structural transformation and build a sophisticated and complex economy continue to be met with significant challenges.

One particular bottleneck for Ghanaian firms seeking to increase production and diversify into knowledge-intensive products is inefficiency at ports and transit points within the Economic Community of West African States (ECOWAS) region. Given that research has shown that improved facilitation may reduce cost and increase trade volumes in a way that far outweighs gains from trade reform, enhancements in transit points could be impactful for Ghana’s economy. Enhancing trade facilitation in the region is paramount if Ghana and countries in the subregion can take full advantage of windfalls associated with a fully operational African Continental Free Trade Area (AfCFTA) agreement, and build their manufacturing sectors.

GHANA’S COMPARATIVE ADVANTAGE

Economic complexity* measures the level of accumulative productive knowledge that exists in an economy—the kind of products a country has strong competencies in making reflects the level of productive knowledge possessed. Complex nations can thus produce more diverse (both simple and sophisticated) products than less complex nations. Ghana’s “economic complexity” level is low, as the products the country has a comparative advantage in are mainly its production of natural resources and agricultural products.

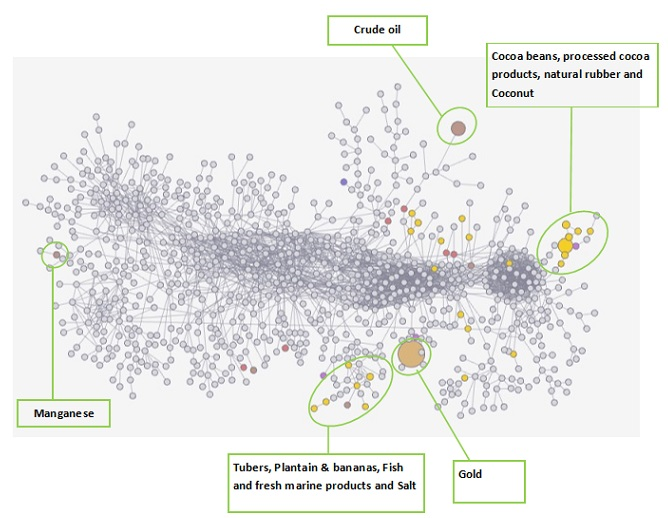

In our recent paper “Economic Complexity and Employment for Women and Youth: The Case of Ghana,” we identify products that could spearhead the diversification of Ghana’s economy using the graphical analytics tool, the product space, which provides a pictorial expression of the productive structure of a country (as an example, Ghana’s product space is shown in Figure 1).

Figure 1. Ghana’s product space, 2015

Source: Figure was generated from the Atlas of Economic Complexity website.

Note: Location of product categories are emphasized by authors.

In this figure, each differently coloured dot represents a product Ghana exports with a comparative advantage. Generally, a product space has two parts, the periphery (represented by loosely connected dots at the fringes) and a core segment (the clustered dots). A country that has a comparative advantage in many products at the core can diversify or structurally transform quickly. Ghana’s product space clearly shows that the country has acquired or built a comparative advantage in products at the periphery—thus transformation is not yet in sight. As a country can only build on already established capabilities, with the help of the product map—alongside other metrics associated with the economic complexity framework—policymakers can identify specific products in which stimulated production can quicken economic diversification.

With the aid of complexity analytics, we identify products that can, when appropriately supported by relevant policies, place Ghana on the right path toward economic transformation. Table 1 provides a list of the top 20 of such (unexplored) products.

Table 1. The Top 20 ‘frontier’ products in Ghana 1 Large flat-rolled iron 11 Glaziers putty 2 Other agricultural machinery 12 Nonaqueous paints 3 Packaged medicaments 13 Soil preparation machinery 4 Other rubber products 14 Styrene polymers 5 Other iron products 15 Raw plastic sheeting 6 Other plastic sheetings 16 Waxes 7 Other printed material 17 Wood crates 8 Nonaqueous pigments 18 Rubber belting 9 Low-voltage protection equipment 19 Aqueous paints 10 Beauty products 20 Shaving products

Source: Compiled using Economic Complexity Dataset.

INEFFICIENCIES AT TRANSIT POINTS AND HOSTILITY AT DESTINATION MARKETS STIFLE GHANA’S STRUCTURAL TRANSFORMATIONAL AGENDA

Now that the products ripe for enhancing Ghana’s economic diversification have been identified, we consider the bottlenecks preventing those products from becoming success cases. Through interviews with firms that are either producing—or possess the capabilities to produce—the 20 products above, we find that these firms face many obstacles in growing and diversifying into other aligned products. Paramount among these is the inefficient trade regime within the ECOWAS subregion. Access to larger markets is therefore beyond reach by local firms at this time.

Throughout the interviews, multiple stakeholders emphasized that the nature of operations at some entry routes hinders efforts aimed at encouraging trade within the subregion, and thus the boosting of Ghana’s economic complexity level. It seems that many firms that make and export identified products that are exportable tariff-free under the ECOWAS Trade Liberalization Scheme (ETLS), find these bottlenecks to be prohibitive. According to the manufacturers, this challenge is exacerbated by steep energy/utilities charges, high interest rates, and numerous taxes, which together push up costs of production.

One top executive explained: “Processing for registration to clear goods that fall under ETLS can take up to six months, as in some cases authorities have doubts about products being made in Ghana, and this heightens hostilities at the ports of entry.” That same executive further remarked that some importers of their products prefer to pay domestic taxes for goods bought, and so find a way of “smuggling” them out of Ghana—rather than export them under ETLS. Another manager recounted his company’s own negative experience: “An export of a container load of tile adhesive by road to Nigeria [was] supposed to reach [the] importer in two days. [It] took two weeks.” A manufacturer of pharmaceutical products expressed dissatisfaction at the level of harassment importers from the ECOWAS subregion faced when distributing and marketing products. In this way, our research indicates that unscrupulous officials and agencies at some ports and access routes in West Africa, through corrupt practices, are often hampering initiatives by companies in Ghana to expand their plants, and are therefore further delaying structural transformation.

KEY RECOMMENDATIONS

As Ghana gears up to take advantage of potential windfalls from the African Continental Free Trade Area (AfCFTA) agreement, the benefits that may accrue will depend on what she exports. At present, the export basket of Ghana comprises mainly products that do not provide the requisite base for structural transformation. Industrial policies and programs such as the One-District One-Factory (1D1F) have emphasized agro-processing industries, but building economic complexity requires ambitious “jumps” to new opportunities. These “jumps” will be successful if they are strategic and feasible (technologically aligned to existing capabilities). If more support (tax reliefs, subsidies, etc.) is given to firms investing, or intending to expand production, in industries that make complex products, Ghana can increase its economic complexity, leading to faster structural transformation. However, without addressing bottlenecks such as delays at ports and other transit points, the country will struggle to meet its potential when it comes to developing a strong manufacturing base. In this way, trade facilitation programs in non-tariff form, such as better customs administration and improved cooperation between export agencies across countries in West Africa, could help reverse this trend.

More broadly, stronger collaborations among ministries of trade and industry of governments in the ECOWAS subregion are needed to firm up tariff-free agreements such as ETLS. The resulting benefits from increased trade volumes in the subregion would not only brighten the finances of individual companies, but will open up quality employment avenues for youth and women seeking decent work.

Source: brookings.edu

Trending News

New train crashes on test run

20:35

Alan launches Alliance for Revolutionary Change (ARC) today

06:02

Engineering Council disgusted by Ashanti ECG MD's arrest on minister's orders

11:20

Bawumia visits Madina market Friday

15:23

Ameri name tainted with NDC’s corruption-NPP

17:04

2024 World Earth Day: Reduce production of all forms of plastic to 60% by 2040 – CCLG-Africa to gov’t’s

10:44

Adu-Ampomah & Amoah know Lithovit is liquid fertiliser – COCOBOD RM&E Dir. tells court

10:26

Man allegedly shoots wife in Adaklu

15:01

Ashanti NDC condemns renaming of Ameri Power Plant

16:55

IMF: Failure to agree Eurobond deal 'won't stop us from providing more financing to Ghana'

08:41